The District Heating Market is estimated to be valued at US$ 50.8 Bn in 2023 and is expected to exhibit a CAGR of 1.5% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights.

Market Overview:

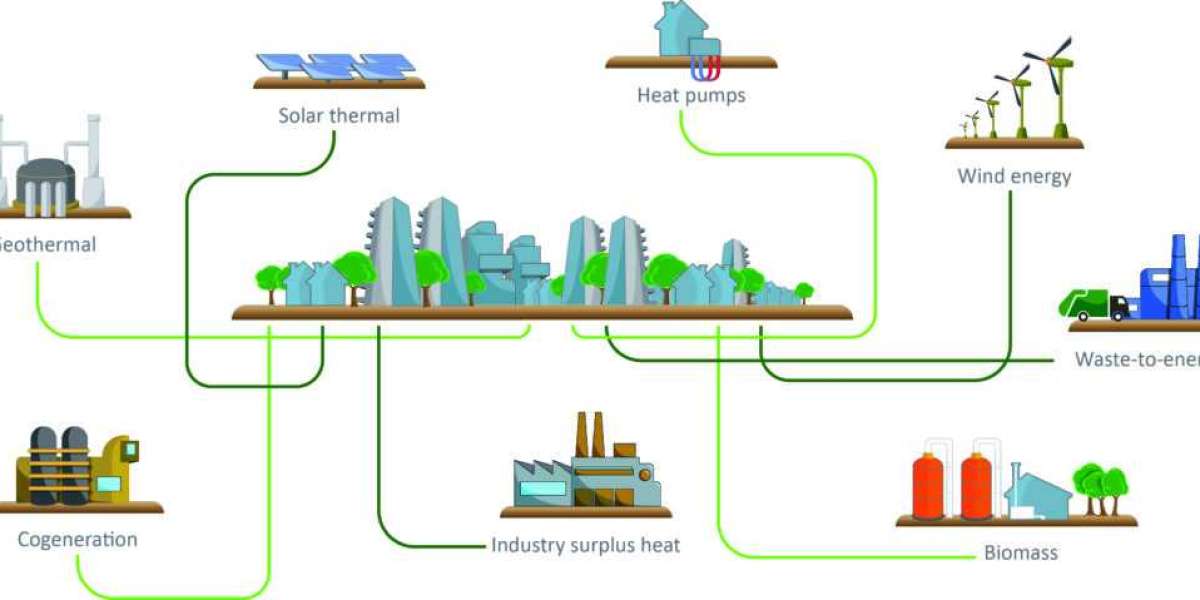

District heating is a system for distributing heat generated in a centralized location through a system of insulated pipes for residential and commercial heating requirements such as space heating and water heating. It involves the production of hot water or steam in a centralized location and distributing it through underground pipelines to residential and commercial buildings for space heating. District heating systems provide an efficient and reliable method of supplying heat especially in densely populated areas. It reduces air pollution and carbon footprints as compared to individual heating systems such as furnaces, boilers etc.

Market key trends:

The global district heating market is expected to witness significant growth owing to rising trends towards sustainable and renewable sources of energy for heating applications. District heating provides an opportunity to use renewable energy sources such as geothermal, biomass, solar thermal, hydro and others for generating heat at centralized locations and supply it to residential and commercial buildings through an underground network of pipes. This helps reduce dependence on fossil fuels for heating needs and lower carbon emissions. Government support through incentives and supportive policies towards implementation of sustainable district energy systems will further propel the market growth over the forecast period.

Porter's Analysis

- Threat of new entrants: The requirement of high initial capital investments and infrastructure development for a district heating network deters new players. However, the threat is moderate due to the increasing focus on renewable energy sources by new ventures.

- Bargaining power of buyers: The bargaining power of buyers is low as district heating is an essential utility service with not many close substitutes available. Switching to alternate heating technologies also requires high investment.

- Bargaining power of suppliers: Fuel and technology providers have moderate bargaining power due to fewer dominant suppliers in the market and different fuel sources that can be utilized for district heating.

- Threat of new substitutes: The threat from renewable substitutes like geothermal and solar thermal is moderate as it may provide an alternative in specific regions.

- Competitive rivalry: High due to the presence of many large players and potential for market expansions.

SWOT Analysis

- Strengths: Environment-friendly, energy efficient and cost-effective heating solution. Ability to utilize waste heat and renewable sources.

- Weaknesses: High initial investments, dependency on weather conditions, public perception challenges.

- Opportunities: Increasing focus on renewable energy targets, expansion opportunities in developing nations.

- Threats: Technology advancements in alternate heating solutions, regulatory hurdles in new projects.

Key Takeaways

The global district heating market is expected to witness high growth at a CAGR of 1.5% over the forecast period, due to increasing investments in renewable energy-based district heating projects across Europe and Asia Pacific.

The European region currently dominates the market with over 50% share due to the strong presence of Nordic countries leading in district heating utilization. However, the Asia Pacific region is estimated to offer lucrative opportunities owing to the rise of smart city projects and growing heating demand in developing economies.

The European region is the fastest growing market for district heating due to strict climate policies and targets. Countries like Sweden, Denmark, Poland and Germany are major contributors with over 80% of their heating from district heating sources. Asia Pacific is also emerging as a promising regional market led by China, Japan and South Korea with increasing infrastructural developments.

Key players operating in the district heating market are Vattenfall AB, SP Group, Danfoss Group, Engie, NRG Energy Inc., Statkraft AS, Logstor AS, Shinryo Corporation, Vital Energi Ltd, Göteborg Energi, Alfa Laval AB, Ramboll Group AS, Keppel Corporation Limited, FVB Energy.